How Much Does Health Insurance Cost in Canada? (2026 Prices)

How much does private health insurance cost in Canada?

A single adult pays between $75 and $150 per month, on average, for private health insurance in Canada. Basic plans with lower reimbursement rates start around $50–$75 per month, while comprehensive plans with dental insurance, prescription drug coverage, and strong paramedical benefits range from around $150 per month to $200 or more.

Age and location are the biggest predictors of health insurance costs after coverage level. Single adults under age 35 pay the lowest rates for private health insurance, while families with children or older adults may see higher premiums overall. Ontario has the highest private health insurance costs of any province, while Saskatchewan has the lowest.

When we say health insurance, we’re talking about private plans, not the government-funded medical coverage that Canadian residents automatically get through their provinces. Private health insurance includes coverage for things that public healthcare doesn’t fully pay for, like prescriptions, dental services, vision care, therapy, etc.

What impacts health insurance costs?

What you pay depends on your personal profile and what kind of coverage you’re looking for. A few key factors will impact how much you pay for private health insurance:

- Your age: The older you are, the higher your premium—especially if you’re over 50.

- Your medical history: Pre-existing conditions can raise costs or exclude you from coverage.

- Where you live: Rates can vary slightly by province based on regional healthcare costs; someone from Ontario will pay different rates than someone from British Columbia or Quebec.

- Your coverage level: More coverage (like adding mental health or comprehensive prescription drugs) means higher premiums.

How much is family health insurance per month?

The typical cost of a family health plan in Canada ranges from $180 to $450 per month, depending on factors like family size, ages, and the level of coverage selected.

Family plans often offer better value per person—especially for households with children. They tend to work best when everyone has similar healthcare needs and you don’t anticipate multiple high-cost claims in the same year.

With a family plan, you get:

- A shared policy that covers everyone in the family

- A single premium with a single deductible

- Shared coverage limits

- Less admin to manage

It’s worth noting that you don’t need children to qualify for a family plan; two adults can enroll in a family plan together. That said, individual plans may make more financial sense if one of you has higher medical needs or partial employer coverage.

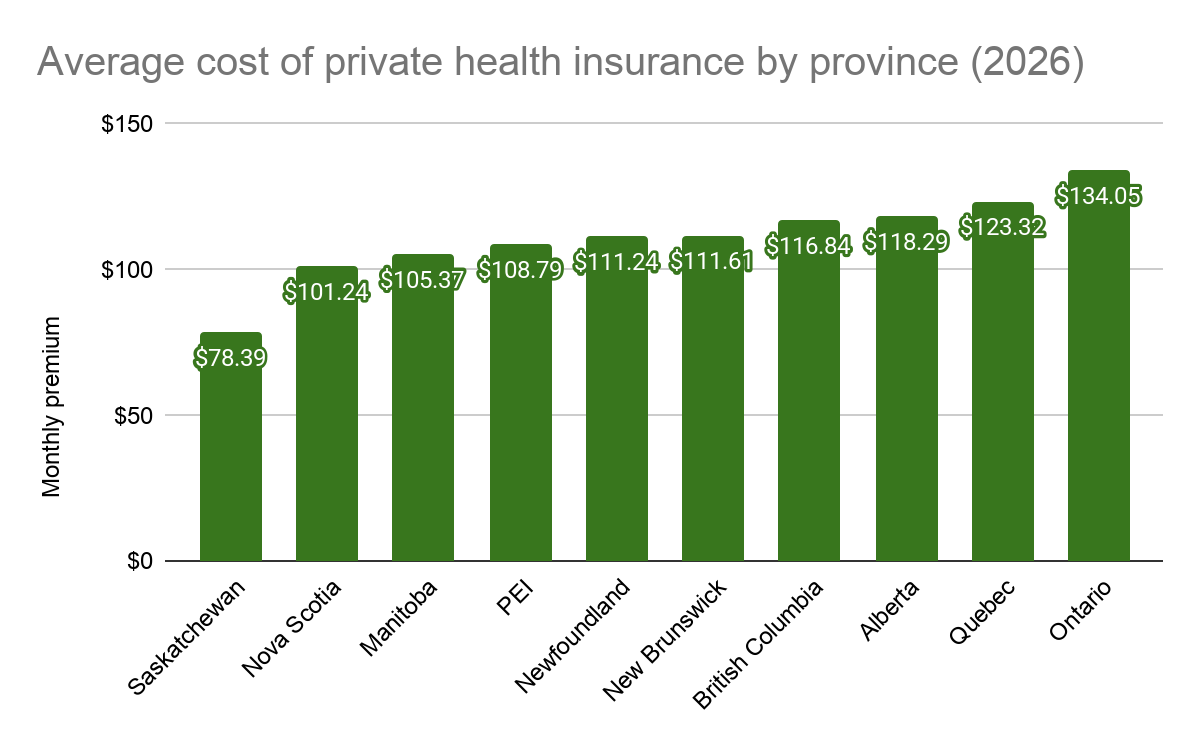

Health insurance cost by province in Canada

Health insurance costs can vary depending on where you live. Differences in provincial healthcare systems and pricing regulations influence the cost of your monthly premiums.

We’ve laid out the average cost for PolicyMe’s Economic plan in each province, for applicants aged 21–44. These give you a clear, apples-to-apples comparison of what basic private health insurance might cost across Canada.

* Premiums may vary and are based on publicly available rates as of May 2026.

Ontario and Quebec consistently have the highest health insurance premiums of any province, while Saskatchewan has the lowest healthcare costs in the nation.

Health insurance cost by age in Canada

Age is one of the biggest factors that impacts your health insurance premium. The older you are, the more you’re likely to pay more for the same level of coverage. Age may also affect eligibility for healthcare coverage, depending on the company’s underwriting.

Below, we’ve laid out starting monthly rates for PolicyMe’s Economic plan in Alberta by age group, so you can get a sense of how pricing changes over time.

* Premiums may vary and are based on publicly available rates as of May 2026.

Health insurance costs can vary significantly for older Canadians, with prices dropping for those in their mid-to-late sixties but rising later in life to account for the higher financial burden to insurers.

Health insurance cost by plan type

The health insurance policy you choose, along with its coverage level, is the next-biggest factor that impacts your premium. To give you an idea of how much your policy might cost based on your plan, we've pulled rates for the PolicyMe health insurance plans Economic, Classic, and Advanced for residents of Saskatchewan.

* Premiums may vary and are based on publicly available rates as of May 2026.

Most young adults can stick to a plan with lower coverage like the Economic plan, while households with children and or those with more significant healthcare needs may want the higher coverage level of the Classic or Advanced plans.

“Compared to individuals, families should prioritize higher coverage limits, strong dental and vision benefits, and things like child-focused care or mental health support. It’s also important to look at how the plan handles claims per person versus per family, since costs can add up quickly. It’s about finding a plan that’s flexible, comprehensive, and built to handle real-life situations, not just the basics.” —Luke Robar, Licensed Insurance Advisor

What is the cheapest health insurance in Canada?

A handful of health insurance plans in Canada fall near or below $100/month for single adults, with the GMS Basic Plan starting as low as $10/month for young adults.

The cheapest health insurance plans in Canada typically come with major tradeoffs in the form of services not covered or low reimbursement rates and caps. The ultra-cheap GMS Basic Plan, for instance, only covers paramedical services and certain emergency costs like ambulance fees; it’s not a good fit for those in search of routine coverage. Sun Life’s Personal Health Insurance Basic Plan covers most supplemental health costs other than vision care, but only reimburses up to 60% of expenses.

A low-cost health insurance plan may be a good fit for you if:

- You’re a single adult in generally good health

- Your routine out-of-pocket healthcare spending is low

- You only use a few services that aren’t covered by public healthcare in your province

- You’re comfortable splitting a large portion of your medical costs with insurance

Is private health insurance worth the cost?

Private health insurance is not a one-size-fits-all decision. For instance, do you already have a group plan or benefits plan available to you at work? If you don’t, private medical insurance may give you that extra peace of mind you need.

To figure out if it’s worth paying for, compare your current healthcare spending with what you’d pay for a plan. Then think about what kind of coverage would actually make your life easier.

Here’s how to break it down:

- Add up your average healthcare costs: Look at what you spend on things like prescription drugs, dental care, glasses, or therapy. Include anything you skipped because it was too pricey. In Canada, prescription spending for private plans has gone up 12.9% since 2023.

- Compare that to the annual cost of a plan: Multiply the monthly premium by 12. If your plan costs $100 a month, that’s $1,200 a year.

- Factor in what the plan would cover: Most plans reimburse between 70–100% of eligible costs. If your expected expenses are higher than the plan’s cost, that’s a net gain.

- Think about what you might avoid without coverage: Would you delay care or skip treatments if you had to pay full price? That can lead to bigger problems and bigger bills down the road.

- Consider the stability a plan gives you: Even if you don’t save money every year, having coverage gives you predictable costs and a buffer against surprise health expenses.

The value of a health plan is not just about saving money—it’s about making care more accessible, staying ahead of issues, and having fewer financial surprises when life throws a curveball. In fact, Canadians claimed more than $32.5 billion in supplementary health benefits in 2022 alone, showing just how often private plans are used for everyday care.

How to find affordable health insurance in Canada

Finding affordable health insurance comes down to choosing the right coverage, comparing providers, and maintaining good health.

Compare providers. Prices can vary widely between insurers, even for similar coverage.

- Get quotes from multiple companies that serve your area and read the fine print.

- Read reviews to understand the customer service experience (cost isn’t everything!).

- Work with an advisor or broker to get the best rate and simplify the shopping process.

Adjust your coverage. Get a plan that covers what you actually need—no more, no less.

- Higher deductibles mean lower monthly premiums, if you can afford the out-of-pocket costs.

- Basic plans reduce coverage but cost less than comprehensive policies.

- Skip dental coverage or pay out of pocket if you need minimal care.

Take care of yourself. Your lifestyle and health status can affect eligibility and pricing for private health insurance plans.

- Quit smoking; nonsmokers get better rates and fewer restrictions.

- Manage chronic conditions to keep your health stable and avoid exclusions.

- Apply now, before you develop conditions that might raise your rates.

Carefully assess your family’s needs to balance cost and coverage. Saving on monthly premiums isn’t worth it if you don’t have the coverage you need when it matters most.

What to compare when looking at quotes from different insurance providers

Price is a major differentiator when comparing individual health insurance plans, but the lowest premium may not mean it’s the best value or the right type of coverage for you.

When comparing health insurance quotes from different companies, be sure to look beyond the monthly rate: What’s the waiting period? What do they cover or not cover? What will you actually pay out of pocket?

The real cost of health insurance depends on these factors.

"Prescription drugs tend to be one of the most frequently used and costly out-of-pocket items, so this coverage offers strong value if you fill multiple prescriptions per year. Using multiple types of services is often when private health insurance really starts to pay off." —Ivana Govedarica, Life Insurance Advisor

How much do you save with private health insurance coverage?

Private health insurance can help you save money if you use it regularly. The amount you save depends on what your plan covers, how often you need care, and what those services would cost you out of pocket.

* Based on typical annual costs for the aforementioned healthcare services in Canada.

** Based on 80% coverage for prescription medication, 80% coverage for dental, bi-annual cap of $200 every two years for vision, and 80% coverage up to a $300 cap for massage and $500 cap for physiotherapy.

Here’s where your savings usually come from:

- Prescription medications: Even with provincial coverage, many people still pay out of pocket. A plan that covers 70% or more of drug costs can save you hundreds per year if you take regular medication.

- Dental care: A basic cleaning can cost around $225. Two visits a year means $300 out of pocket. If you need a filling or x-ray, the total jumps quickly. Most private plans cover 80% of routine dental care. The CDCP may cover dental insurance for some Canadians, but it’s not comprehensive.

- Vision care: Glasses or contacts often cost between $200 and $400 every couple of years. A plan with vision coverage helps bring that number down.

- Paramedical services: This includes physiotherapy, massages, chiropractic care, or counselling. If your plan covers 80% per visit, your savings can grow fast—especially if you use these services more than a few times a year.

- More predictable costs: Even if what you claim in a year equals your premium, you’re swapping unpredictable bills for one steady monthly cost. That kind of consistency can reduce financial stress.

Saving money is one thing; being able to afford care when you need emergency medical care is another. According to PolicyMe’s recent survey, 56% of Canadians are delaying or skipping health appointments because of cost. A private health insurance plan can take the pressure off, so you’re not forced to choose between your budget and your well-being.

Want to see it for yourself? Add up what you spent on medical services last year. Then compare it to the cost of a plan and what would have been reimbursed. In many cases, the savings are clear. And even when they’re not, the value is knowing care is within reach when you need it.

Cutting the cost of health insurance through tax deductions

Private insurance in Canada might feel like a big expense, but some of that cost could come back to you at tax time. The more you’ve spent on your healthcare needs in a year, the more helpful the credit becomes.

You may be able to claim the premiums you pay for private health insurance as a medical expense on your tax return if your plan includes:

- Prescription drug coverage

- Dental coverage

- Vision coverage

- Paramedical services

These qualify under the CRA’s list of eligible medical expenses. Other types of private health coverage, like travel insurance, may not qualify.

Here’s how to get the tax credit for personal health insurance costs:

- Total up your total medical expenses for the year.

- Find out if it exceeds either three percent of your net income or a fixed amount set by the CRA, whichever is lower. For the 2025 tax year, that fixed amount is $2,834.

- Fill out lines 33099 and 33199 on your tax return.

- Get credit for the portion of expenses that goes over this threshold.

Note that this is a non-refundable tax credit. It won’t give you a refund, but it can reduce the amount of tax you owe. So while it won’t wipe out the cost of your premiums, it can take the edge off—especially when combined with other eligible health expenses.

The bottom line on health insurance costs

Health insurance costs can add up, but they can also prevent even bigger out-of-pocket surprises—especially if you’re using services like dental, prescriptions, or physio regularly.

If you're comparing quotes, focus on total value, not just the monthly rate. Small details like claim limits and waiting periods can make a big difference.

The best health insurance plan is one that fits your needs, your budget, and your stage of life, not just the one with the lowest premium.

FAQ: How much does health insurance cost

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.

Bonnie Stinson is an insurance writer and researcher in Toronto with a decade of experience producing helpful, accurate content for Canadians. They have published resources for some of Canada's most innovative and consumer-trusted companies in the health, legal, and fintech sectors.

Prices listed on this page are based on information available as of March 2026. The prices shown are for general reference only and may vary based on factors like your age, location, and product selection.